Are you ready to discuss the final ECB NPL Guidance with your Joint Supervisory Team?

Are you ready to discuss NPLs?

The ECB finalised its NPL Guidance on 20 March 2017

On March 20, the ECB published the final guidance (PDF 1.98 MB) to banks on non-performing loans (NPLs). The guidance, published as a draft in September last year, was subject to a two month consultation phase and a public hearing (see the webcast). According to the ECB, the guidance should be applied starting with its date of publication, meaning that the guidance effectively has entered into force. From meetings with banks over the last couple of weeks, we expect the quick entry into force will be a surprise for some banks, since they expected an explicit transitional period.

Shift in emphasis from proportionality to universal application

The final guidance contains further clarifications on its applicability, effectively broadening this beyond the ‘usual’ suspects on the NPL topic. As an example, the ECB clarified in the accompanying feedback statement (PDF 260 KB), that even for a ‘low NPL bank’ the sections on NPL Strategy and Governance and Operations (and the respective annexes) can be applicable to certain parts of the business such as sectoral/regional portfolios or subsidiaries higher NPL levels if deemed appropriate by the JST.

This relativizes the previous discretionary distinction between high (and low) NPL banks, by shifting the debate from bank-level towards portfolio-level application. The ECB also clarified that not only NPLs but also foreclosed assets or watch lists could trigger banks being classified as a high NPL bank. Furthermore, the ECB clarified that all significant institutions are expected to implement effective early warning mechanism as suggested in the Guidance. Taken together, these changes shift the emphasis further towards universal application for all significant institutions.

Few changes to substance compared with the consultation draft

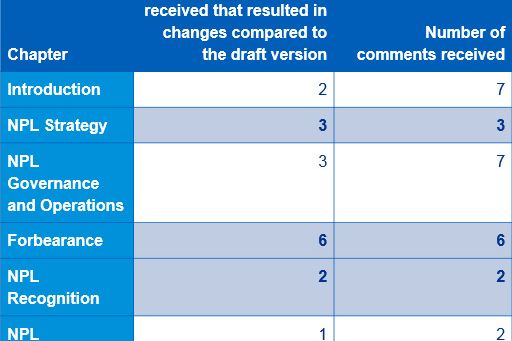

As expected (see February article), the final draft includes overall few changes. In the final version, the ECB clarified that an assessment of banks’ NPL-management will be part of the annual SREP cycle, implying indirectly Pillar 2 requirements for non-compliance. The ECB also clarified that the NPL disclosure expectations described in the guidance should be implemented beginning with 2018 reference dates onwards. With regards to each chapter, the number of effective changes due to the comments received varies (see table 1). As an example, all comments received for the chapters on NPL Strategy, Forbearance and NPL Recognition resulted in changes of the guidance, while not all comments received on other chapters resulted in final version changes.

Table 1: Overview on comments received and effective changes of the draft guidance by chapter. Source: ECB.

In the following, we shortly highlight selected changes for each chapter of the guidance:

NPL Strategy

- Role of market conduct and consumer protection rules now considered in more detail (i.e. regulatory, legal and judicial framework).

- Expectations for NPL risk transfers, incl. securitizations, specified in more detail (new paragraph and new annex 8 explicitly on NPL risk transfer included).

- NPL reduction targets now also required to be aligned with (more granular) operational targets.

NPL Governance and Operations

- Regular feedback loops and smooth flow of information between credit units and NPL workout units (WU’s) further emphasized.

- Minimum monitoring period specified for forborne exposure for transfer out the NPL WUs (at least one year in line with EBA’s probation cure period definition).

- Explicit veto right for risk control functions included to ensure independence of the risk control function and sufficient power to intervene in risk-related decision-making

Forbearance

- Clarification of potential need to review contractual terms of forbearance measures in case of an improvement of the borrower situation.

- Multiple forbearance measures now explicitly need the attention of the risk control function (ex-ante) and the explicit approval of the relevant senior decision-making body (e.g. NPL committee).

- Strict requirement for no other short-term forbearance measure to have been applied in the past to the same exposure has been deleted.

- Long-term forbearance measures may include also short-term measures (e.g. interest only, reduced payments, grace period or arrears capitalization for a limited timeframe).

- No automatic classification of the respective exposure as “forborne” in case of taking additional security.

- Focus of the list of elements to analyze borrower affordability has been broadened (analysis of cash-flow and business plans added)

NPL recognition

- Clarification on the potential ambiguity in EBA’s cure definition and respective criteria (to avoid “window dressing”).

- Clarification that when IFRS 9 comes into force, at least all Stage 3 exposures are expected to be subject of this NPL guidance

NPL measurement

- Time horizon for the estimation of operating cash flows reduced to a minimum of five years (instead of ten years, but 10 years still admissible in exceptional circumstances).

Collateral valuations

- Some aspects including the frequency of reviewing valuations for performing vs. non-performing exposures have been clarified.

- Rotation requirement clarified to be applied to individual appraisers (internal valuation) and at firm level (external appraiser).

- Use of mortgage lending value (in addition to market value) included as an option to value immovable property collateral (to ensure consistency with CRR).

- Back-testing requirement further aligned with IFRS 9 (in particular for cases of indexation).

High volume of feedback from the sector compared to other SSM consultations

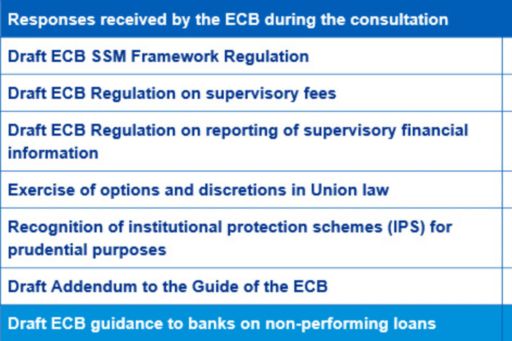

In total, the ECB received 44 responses during the consultation phase. Compared to other consultations (see table 2), the number received for the NPL Guidance is the highest – an indication of its impact on the sector, and on multiple stakeholders within each SSM supervised bank.

Table 2: Overview on comments received during consultation phases (non-exhaustive). Source: ECB.

Defending conservatism

Not surprisingly, the ECB also defended the notion of “conservatism” and “prudence” used in the NPL guidance, which are sometimes regarded by market participants as being incompatible with accounting standards (general requirement for neutrality under the IFRS Framework). In response to that, the ECB is “firmly of the view that in areas of uncertainty requiring management judgement a management bias exists and, therefore, a level of conservatism is required to ensure that a neutral view is attained”. We understand the ECB will want to see this logic applied in particular to NPL provisioning in “areas of uncertainty”.

Gap analysis and action plan – what banks should do now

The NPL guidance has de facto entered into force. Significant institutions are now expected to comply with the principles and expectations laid down in the guidance, subject to the proportionate judgement of their Joint Supervisory Team (JST). Banks with NPLs in their portfolios are therefore well advised to analyze potential gaps of their NPL management compared to ECB’s guidance; they should also immediately develop action plans to be prepared for the discussion with their JST and the next Supervisory Review and Evaluation Process (SREP) cycle.

Our KPMG gap analysis tool on ECB’s NPL guidance allows banks to quickly identify potential areas of non-compliance and helps to develop an action plan to ensure compliance over time. From banks’ perspective, it is now also crucial to clearly identify interdependencies with current implementation projects (e.g. IFRS 9, CRR default definition, BCBS 239), optimize necessary implementation costs and align their project activities needed to ensure compliance with the guidance.

For further details on this topic, please contact Marcus Evans (Marcus.Evans@KPMG.co.uk) or David Nicolaus (DNicolaus@kpmg.com) from KPMG’s ECB Office.